Image courtesy: Agito Medical

Medical imaging services and maintenance revenue to reach $23 billion by 2029

April 02, 2025

By Poornima Anil

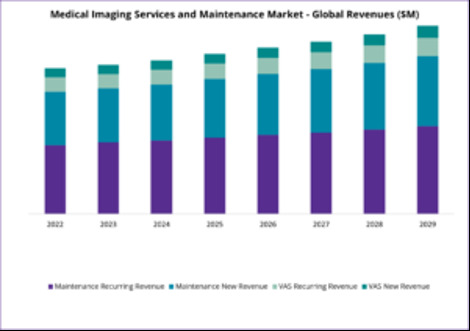

According to Signify Research's latest report, the Medical Imaging Services and Maintenance market is projected to exceed $23 billion by 2029. This growth is driven by increased uptake for services in key modalities such as MR, CT, and interventional X-ray systems, which have high maintenance and service contract penetration rates.

The medical imaging sector is currently navigating a landscape marked by heightened geopolitical and macroeconomic challenges. The ongoing shortages of skilled staff and the growing need to enhance workforce efficiency are further fueling the expansion of the value-added services market. In response, imaging vendors are broadening their offerings, providing a variety of services, from providing training and workforce management to fleet management, designed to improve economic outcomes and operational efficiency for healthcare providers.

Minimizing downtime and enhancing patient throughput have become critical priorities for healthcare providers. There is an increased preference for predictive maintenance and remote diagnostics and repairs to proactively address potential issues, reducing reliance on on-site visits. This approach not only maximises system uptime but also ensures that medical equipment remains fully operational when it's needed most, ultimately improving patient care.

Moreover, procurement decisions are increasingly based on Total Cost of Ownership (TCO) rather than just the initial equipment or service costs. Healthcare providers are evaluating OEMs on the long-term costs, including service contracts and maintenance expenses, which influence their purchasing decisions. With the growing installed base of imaging equipment, healthcare facilities are placing more value on comprehensive maintenance contracts to ensure reliability, compliance, and access to specialized expertise.

Rise in recurring revenue models

The medical imaging industry is witnessing a pronounced shift toward recurring revenue models, driven by both OEM strategies and healthcare facility preferences. Budget constraints and economic volatility are pushing healthcare facilities to favour multiyear maintenance agreements, seeking cost predictability and risk mitigation. OEMs, in turn, are driving this adoption by transitioning into turnkey solution providers, offering comprehensive packages that include equipment, installation, and ongoing support. This strategy secures predictable income and fosters long-term customer partnerships.

Bundled service offerings enhance customer loyalty, creating a competitive advantage through integrated service ecosystems and fostering long-term customer engagement. Ultimately, strong vendor-payer collaborations will be critical to delivering optimal patient outcomes and improved healthcare value. Evidence of this trend is significant, with major players already generating substantial recurring revenue, and others planning to increase service-based income.

Regional growth influenced by value partnerships and cost-effective contracts

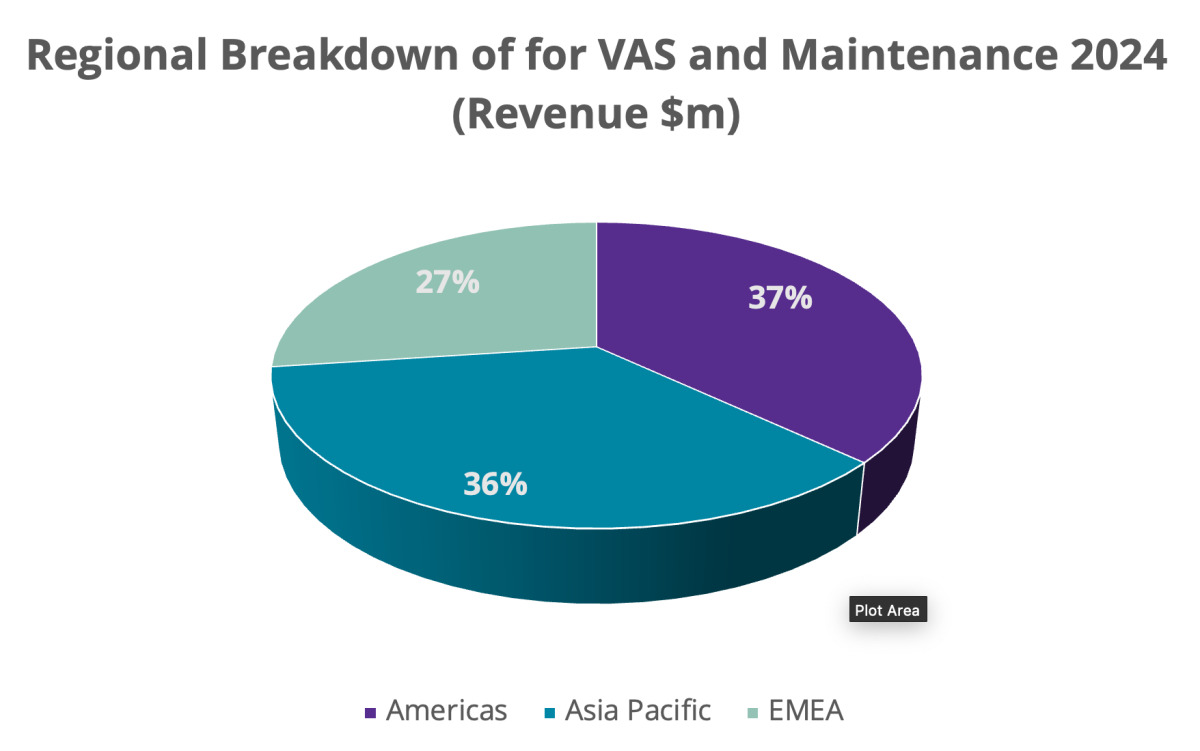

The growth of the services and maintenance market will be primarily driven by the Asia Pacific region, particularly due to the lack of servicing contracts at present. The region is witnessing a surge in third-party maintenance providers, particularly in India, where cost sensitivity drives demand for cheaper alternatives.

In North America, the industry is shifting toward long-term partnerships, particularly with Integrated Delivery Networks (IDNs) and large hospital groups. This has led to a rise in multimodality service contracts and value-added agreements, ensuring stable, recurring revenue for vendors. However, third-party maintenance providers are gaining traction, particularly for midrange equipment like CT and ultrasound, as healthcare providers seek cost-effective alternatives once initial OEM contracts expire.

Similarly, Western Europe is seeing increased interest in value-added services like education and workflow optimization, though adoption varies across countries. Financial constraints in Germany and Southern Europe are leading hospitals to seek more budget-conscious service solutions.

In Latin America, cost pressures are driving hospitals to explore alternatives to traditional OEM service contracts. The presence of international OEMs remains strong in high-end imaging services, but demand for refurbished equipment and lower-cost maintenance plans is rising.

Technology evolution driving market growth

The integration of Internet of Things (IoT), Digital Twins, and Virtual Reality (VR) is reshaping medical imaging services and maintenance. IoT facilitates continuous, real-time monitoring of imaging devices, offering valuable insights into equipment performance and identifying potential issues before they escalate. This capability supports predictive maintenance, allowing for early fault detection and minimizing unplanned downtime. Digital Twin technology, by creating virtual replicas of imaging equipment, empowers technicians to simulate potential failures, forecast issues, and optimize maintenance schedules, ultimately enhancing system reliability and uptime. Meanwhile, Virtual Reality is proving to be an invaluable tool for technician training and the education of medical professionals, enabling immersive, simulation-based environments for procedure planning and skill development. Together, these technologies streamline maintenance processes, reduce costs, and enhance the overall quality of care delivered to patients.

The advantage of companies who enter first

The current services and maintenance market is primarily dominated by large OEMs and established third-party maintenance service providers (TPMs). However, other vendors are expected to gradually enter this space, bringing new competition. To improve market share opportunities, companies need to consider offering extended warranties, flexible and cost-effective contracts, providing multimodality support, and utilizing advanced predictive technologies. By leveraging these technologies, vendors can proactively address maintenance needs and acquire long-term recurring contracts.

In some cost-sensitive markets, however, the penetration of TPM providers is expected to increase 3-5 years after installation. In the initial years, TPM providers face challenges due to a lack of expertise and limited access to spare parts. Additionally, the complexity of medical systems and the restricted access often imposed by OEMs make it difficult for TPMs to effectively enter the market. Despite these hurdles, over time, as equipment ages and maintenance needs evolve, TPM providers are likely to gain a foothold, offering more cost-effective alternatives to traditional OEM services.

Future of the services and maintenance market

Though the services and maintenance market has high growth potential, it faces significant challenges, including cost pressures, regulatory hurdles, regional differences in digital infrastructure, and a lack of concrete evidence on the effectiveness of certain services. To navigate these obstacles, companies need to invest in innovative solutions, ensure compliance with varying regulations, and adapt to regional infrastructure capabilities. Additionally, they must focus on building a strong evidence base to demonstrate the value and effectiveness of their services, ultimately gaining the trust of healthcare providers and ensuring long-term growth in the market.

About the author: Poornima Anil joined Signify Research’s Medical Imaging Team in 2023. She brings over 14 years of experience in healthcare market research, analysis and business intelligence. She has a master’s degree in bioinformatics and a degree in agriculture and plant science.

About the author: Poornima Anil joined Signify Research’s Medical Imaging Team in 2023. She brings over 14 years of experience in healthcare market research, analysis and business intelligence. She has a master’s degree in bioinformatics and a degree in agriculture and plant science.

Signify Research’s Medical Imaging team formulates expert market intelligence for some of the leading Ultrasound, CT, MR, and X-ray vendors. Combining primary data collection and in-depth discussions with industry stakeholders, our thorough research approach yields credible quantitative and qualitative analysis, helping our customers make critical business decisions with confidence. Furthermore, our commitment to seeking a plurality of perspectives across the markets we cover guarantees that our insights remain independent and balanced.

Signify Research provides health tech market intelligence powered by data that you can trust. We blend insights collected from in-depth interviews with technology vendors and healthcare professionals with sales data reported to us by leading vendors to provide a complete and balanced view of the market trends. Our coverage areas are Medical Imaging, Clinical Care, Digital Health, Diagnostic and Lifesciences and Healthcare IT.

According to Signify Research's latest report, the Medical Imaging Services and Maintenance market is projected to exceed $23 billion by 2029. This growth is driven by increased uptake for services in key modalities such as MR, CT, and interventional X-ray systems, which have high maintenance and service contract penetration rates.

The medical imaging sector is currently navigating a landscape marked by heightened geopolitical and macroeconomic challenges. The ongoing shortages of skilled staff and the growing need to enhance workforce efficiency are further fueling the expansion of the value-added services market. In response, imaging vendors are broadening their offerings, providing a variety of services, from providing training and workforce management to fleet management, designed to improve economic outcomes and operational efficiency for healthcare providers.

Minimizing downtime and enhancing patient throughput have become critical priorities for healthcare providers. There is an increased preference for predictive maintenance and remote diagnostics and repairs to proactively address potential issues, reducing reliance on on-site visits. This approach not only maximises system uptime but also ensures that medical equipment remains fully operational when it's needed most, ultimately improving patient care.

Moreover, procurement decisions are increasingly based on Total Cost of Ownership (TCO) rather than just the initial equipment or service costs. Healthcare providers are evaluating OEMs on the long-term costs, including service contracts and maintenance expenses, which influence their purchasing decisions. With the growing installed base of imaging equipment, healthcare facilities are placing more value on comprehensive maintenance contracts to ensure reliability, compliance, and access to specialized expertise.

The medical imaging industry is witnessing a pronounced shift toward recurring revenue models, driven by both OEM strategies and healthcare facility preferences. Budget constraints and economic volatility are pushing healthcare facilities to favour multiyear maintenance agreements, seeking cost predictability and risk mitigation. OEMs, in turn, are driving this adoption by transitioning into turnkey solution providers, offering comprehensive packages that include equipment, installation, and ongoing support. This strategy secures predictable income and fosters long-term customer partnerships.

Bundled service offerings enhance customer loyalty, creating a competitive advantage through integrated service ecosystems and fostering long-term customer engagement. Ultimately, strong vendor-payer collaborations will be critical to delivering optimal patient outcomes and improved healthcare value. Evidence of this trend is significant, with major players already generating substantial recurring revenue, and others planning to increase service-based income.

Regional growth influenced by value partnerships and cost-effective contracts

The growth of the services and maintenance market will be primarily driven by the Asia Pacific region, particularly due to the lack of servicing contracts at present. The region is witnessing a surge in third-party maintenance providers, particularly in India, where cost sensitivity drives demand for cheaper alternatives.

In North America, the industry is shifting toward long-term partnerships, particularly with Integrated Delivery Networks (IDNs) and large hospital groups. This has led to a rise in multimodality service contracts and value-added agreements, ensuring stable, recurring revenue for vendors. However, third-party maintenance providers are gaining traction, particularly for midrange equipment like CT and ultrasound, as healthcare providers seek cost-effective alternatives once initial OEM contracts expire.

Similarly, Western Europe is seeing increased interest in value-added services like education and workflow optimization, though adoption varies across countries. Financial constraints in Germany and Southern Europe are leading hospitals to seek more budget-conscious service solutions.

In Latin America, cost pressures are driving hospitals to explore alternatives to traditional OEM service contracts. The presence of international OEMs remains strong in high-end imaging services, but demand for refurbished equipment and lower-cost maintenance plans is rising.

Technology evolution driving market growth

The integration of Internet of Things (IoT), Digital Twins, and Virtual Reality (VR) is reshaping medical imaging services and maintenance. IoT facilitates continuous, real-time monitoring of imaging devices, offering valuable insights into equipment performance and identifying potential issues before they escalate. This capability supports predictive maintenance, allowing for early fault detection and minimizing unplanned downtime. Digital Twin technology, by creating virtual replicas of imaging equipment, empowers technicians to simulate potential failures, forecast issues, and optimize maintenance schedules, ultimately enhancing system reliability and uptime. Meanwhile, Virtual Reality is proving to be an invaluable tool for technician training and the education of medical professionals, enabling immersive, simulation-based environments for procedure planning and skill development. Together, these technologies streamline maintenance processes, reduce costs, and enhance the overall quality of care delivered to patients.

The advantage of companies who enter first

The current services and maintenance market is primarily dominated by large OEMs and established third-party maintenance service providers (TPMs). However, other vendors are expected to gradually enter this space, bringing new competition. To improve market share opportunities, companies need to consider offering extended warranties, flexible and cost-effective contracts, providing multimodality support, and utilizing advanced predictive technologies. By leveraging these technologies, vendors can proactively address maintenance needs and acquire long-term recurring contracts.

In some cost-sensitive markets, however, the penetration of TPM providers is expected to increase 3-5 years after installation. In the initial years, TPM providers face challenges due to a lack of expertise and limited access to spare parts. Additionally, the complexity of medical systems and the restricted access often imposed by OEMs make it difficult for TPMs to effectively enter the market. Despite these hurdles, over time, as equipment ages and maintenance needs evolve, TPM providers are likely to gain a foothold, offering more cost-effective alternatives to traditional OEM services.

Future of the services and maintenance market

Though the services and maintenance market has high growth potential, it faces significant challenges, including cost pressures, regulatory hurdles, regional differences in digital infrastructure, and a lack of concrete evidence on the effectiveness of certain services. To navigate these obstacles, companies need to invest in innovative solutions, ensure compliance with varying regulations, and adapt to regional infrastructure capabilities. Additionally, they must focus on building a strong evidence base to demonstrate the value and effectiveness of their services, ultimately gaining the trust of healthcare providers and ensuring long-term growth in the market.

Poornima Anil

Signify Research’s Medical Imaging team formulates expert market intelligence for some of the leading Ultrasound, CT, MR, and X-ray vendors. Combining primary data collection and in-depth discussions with industry stakeholders, our thorough research approach yields credible quantitative and qualitative analysis, helping our customers make critical business decisions with confidence. Furthermore, our commitment to seeking a plurality of perspectives across the markets we cover guarantees that our insights remain independent and balanced.

Signify Research provides health tech market intelligence powered by data that you can trust. We blend insights collected from in-depth interviews with technology vendors and healthcare professionals with sales data reported to us by leading vendors to provide a complete and balanced view of the market trends. Our coverage areas are Medical Imaging, Clinical Care, Digital Health, Diagnostic and Lifesciences and Healthcare IT.