By Mustafa Hassan

Much of the focus in the ultrasound market in the last few years has been on the handheld market. This is justified, considering its role in the response to the COVID-19 pandemic and the spate of innovation in the sector, both in terms of new product releases and partnerships. As a result, there is less mention of the other ultrasound product segments, especially the compact market. However, the compact market has also been active, with the release of Fujifilm SonoSite’s SonoSite LX in February 2022 the latest in a slew of new compact ultrasound releases following the launch of Mindray’s TE7 Max in October 2021 and the release of the SonoSite PX by Fujifilm SonoSite, Venue Fit by GE Healthcare and the SONIMAGE HS2 by Konica Minolta in the last 12-18 months. This raises the question: what role do compact systems have in the ever-changing ultrasound market? What risk does the growing handheld market pose? And what does the future hold for the compact ultrasound market?

Bigger can be better for vendors

Ad Statistics

Times Displayed: 364749

Times Visited: 21098 MIT labs, experts in Multi-Vendor component level repair of: MRI Coils, RF amplifiers, Gradient Amplifiers Contrast Media Injectors. System repairs, sub-assembly repairs, component level repairs, refurbish/calibrate. info@mitlabsusa.com/+1 (305) 470-8013

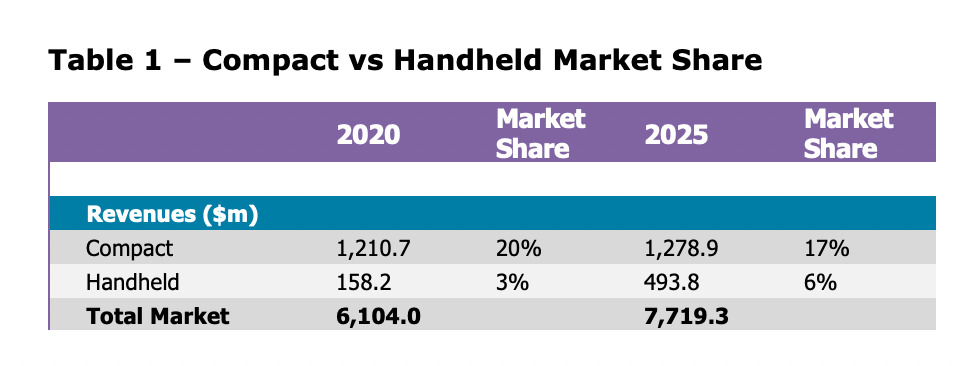

The handheld market is forecast to be the fastest growing product segment, with our

Ultrasound World Market 2021 Report predicting a 2020 to 2025 CAGR of 26%. The lower price of handhelds compared to compact systems means they are attractive to new users who are not experienced in ultrasound. They are also desirable for existing ultrasound customers who want even more portability with their ultrasound systems. The faster pace of AI innovation in handheld systems, with capabilities such as image capture guidance, anatomy detection and image analysis now coming to market, also help make these products more useable for clinicians who are less familiar with ultrasound. This ultimately means that handhelds are, to some extent, taking share from the compact market. However, the handheld market still only accounted for 3% of the global ultrasound market revenues in 2020 (Table 1). This is a mere slice compared to the 20% held by the compact market. Even though the handheld market is forecast to be the fastest-growing product type, driven by its role as an adjunct to existing ultrasound users and penetration into new markets, it will still only account for 6% of the total market in 2025. This is still nearly three times less than the 16% market share forecast for the compact market in that year.

The disparity between the revenue to be gained from compact versus handheld systems is even bigger when considering the aftersales of transducers. Whereas handheld systems are usually sold with a single or dual-probe configuration, with no aftersales of probes, compact ultrasound systems are typically sold with 2 or 3 transducers, with the prospect of additional or replacement probe sales in the future. This comes at an additional cost and pushes up the average selling price vendors can achieve. The SonoSite LX is a prime example of this. Alongside the launch of the new system, it launched a new T8-3 transoesophageal transducer, designed to be used with the SonoSite LX and SonoSite PX. The addition of a high-value, specialist probe not only increases the initial price of the system, but customers may need to purchase another T8-3 before replacing the SonoSite LX. Our report

Ultrasound Transducers & Catheters – World Market – 2021 Edition shows the average selling price (ASP) for transducers to be around $3,500 (heavily discounted due to bulk sales of transducers with ultrasound systems). This means transducers can easily add $7-$10k on top of the price of a compact ultrasound system, potentially more depending on the transducer types. Furthermore there are typically more opportunities to upsell services and software with compact systems than with handhelds.