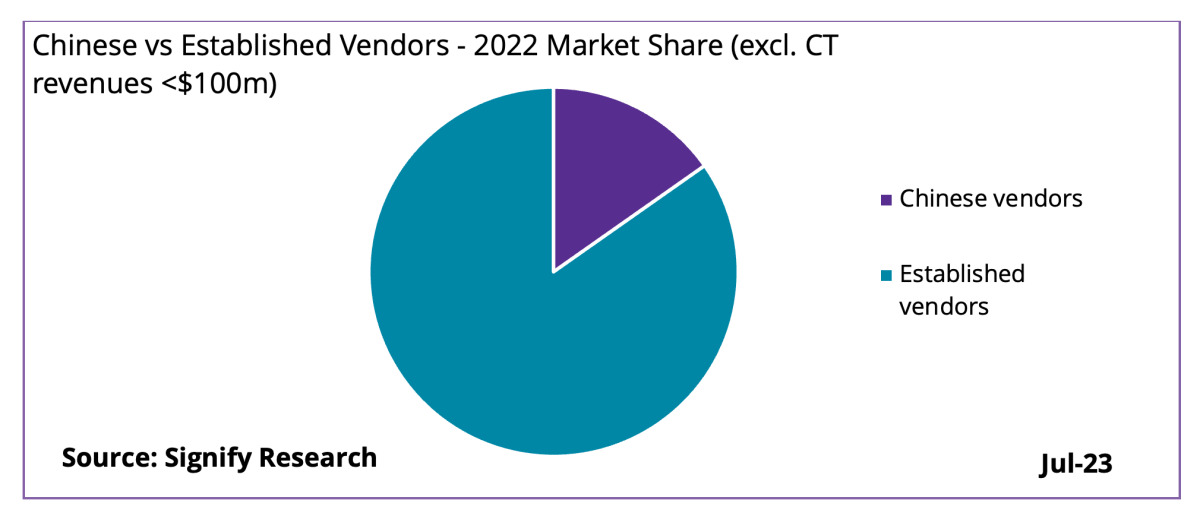

Chinese vendors poised for more traction

While 2022 represented a lacklustre year for China-based vendors, owing mainly to disruption from local lockdown measures, the challenge they pose to established competitors will likely intensify over the medium term. In addition to steady market share gains domestically, United Imaging and Neusoft have made concerted efforts to break into new geographies in recent years. United Imaging, for instance, entered the U.S. market in 2018, and its aggressive overseas sales strategy has recently netted the company novel installations in Western Europe. Critical to their success has been undercutting on price, without forfeiting technical features, and sizable government subsidies.

However, hurdles other than sustaining price erosion lie ahead if Chinese vendors wish to expand their global reach. One disadvantage is the gap in R&D spending between themselves and rivals Siemens Healthineers, GE HealthCare, and Canon Medical. Such a disparity leaves cutting-edge technological innovation out of scope and could see Chinese companies lose out as their peers continue to strengthen their photon-counting CT and AI offerings — technologies which could, provided the right amount of investment, heighten market expansion and lead to new clinical opportunities. Another more immediate barrier is a lack of brand awareness, credibility, and loyalty in mature geographies. This is further exacerbated by evolving purchasing models that increasingly include life cycle support services for multimodality fleets. A critical question for Chinese vendors in the near term is how to establish a reliable network of personnel to provide these services responsively.

Ad Statistics

Times Displayed: 21862

Times Visited: 433 Stay up to date with the latest training to fix, troubleshoot, and maintain your critical care devices. GE HealthCare offers multiple training formats to empower teams and expand knowledge, saving you time and money

Much more on the horizon

A combination of both the expanded clinical and technological opportunities indicate a robust market outlook for CT equipment over the forecast period. In the medium-long term, the enduring clinical relevance of CT will likely be expanded upon as providers take advantage of PCCT and AI, particularly in already established markets. The Chinese market, the largest globally, is expected to see a decisive shift to mid-range and premium investment in the wake of recent licensing changes. Other trends to monitor include the growth of outpatient settings amid reimbursement challenges, market cannibalisation of other modalities, such as high-end DR, and the pace of CT-enabling infrastructure development in emerging markets, including imaging facilities and PACS architecture.

About the author: Matthew Watson joined Signify Research in 2022 as part of the Medical Imaging team. He holds a first-class MA degree in Economics, graduating from Heriot-Watt University in 2022, and previously worked as an intern at Unilever. Signify Research provides healthtech market intelligence powered by data that you can trust. We blend insights collected from in-depth interviews with technology vendors and healthcare professionals with sales data reported to us by leading vendors, to provide a complete and balanced view of the market trends. Our coverage areas are Medical Imaging, Clinical Care, Digital Health, Diagnostic and Lifesciences and Healthcare IT.Back to HCB News