Consistent with the tagline of a Liberty Mutual commercial, employers should offer and workers should select coverage so everyone ‘only pays for what they need.’ Excluding Medicare-eligible Americans (age 65+ and disabled), health expenditure data suggest that over 80% of Americans with employer-sponsored coverage spend less than $1,000 a year on medical services.

The HSA marketplace

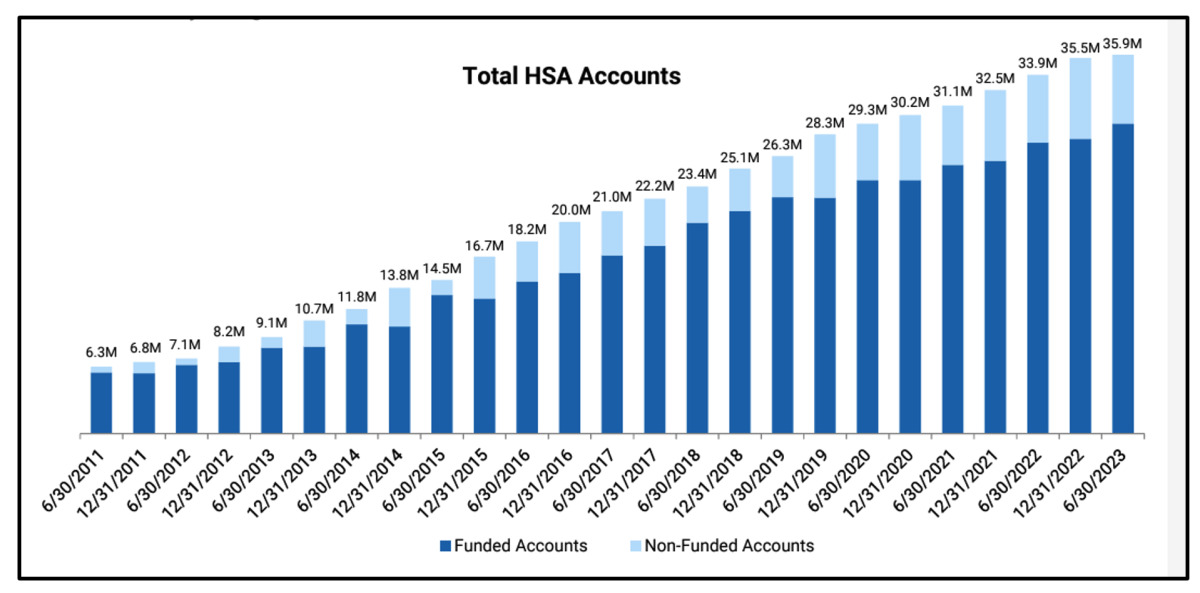

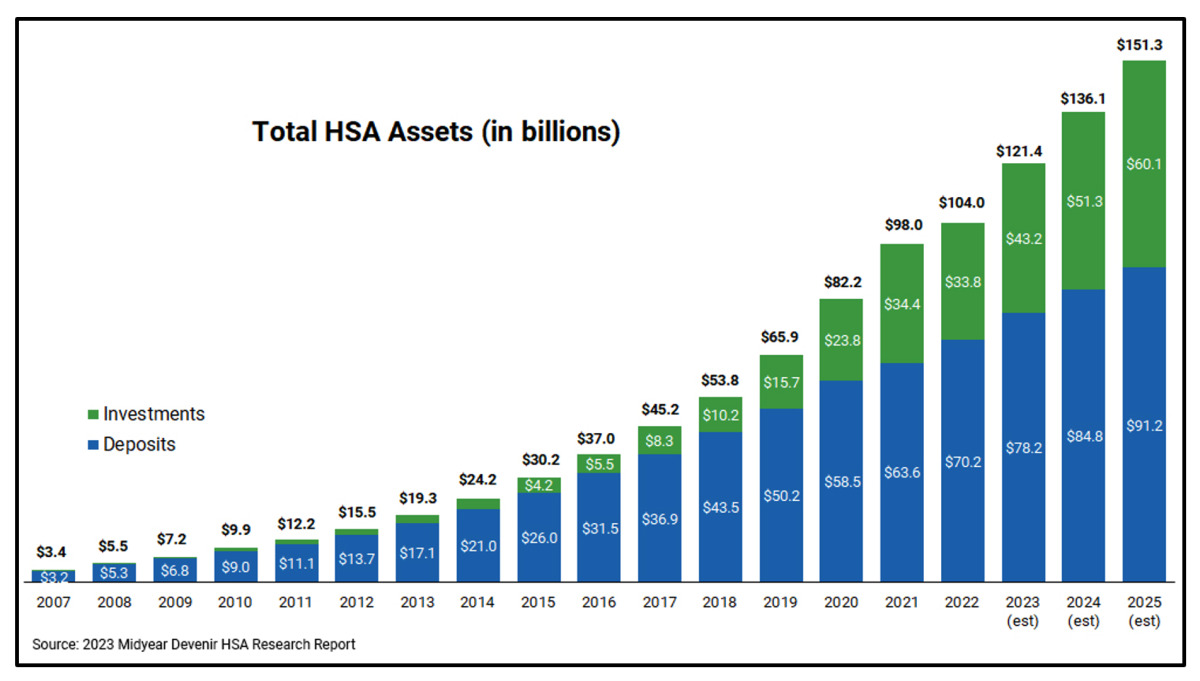

Starting from zero, we’ve seen dramatic growth in the number of HSA accounts and assets. It looks impressive, but it only represents a small percentage of America’s employers and their workers. Consider the mid-year 2023 Devenir report:

Ad Statistics

Times Displayed: 79541

Times Visited: 2807 Ampronix, a Top Master Distributor for Sony Medical, provides Sales, Service & Exchanges for Sony Surgical Displays, Printers, & More. Rely on Us for Expert Support Tailored to Your Needs. Email info@ampronix.com or Call 949-273-8000 for Premier Pricing.

HSA Account Growth: Midyear 2023, there were 36 million HSA Accounts, a year-over-year 6% increase.

Growth in Assets: Midyear 2023, there were $116 billion in HSA assets, a year-over-year 17% increase.

Lack of Investing: However, a super-majority of HSA accounts are invested only in capital preservation investments/deposits.

When you drill down into the data, the significance of the missed opportunity is apparent - including the following trends:

• HSA Participation: Only 50% of eligibles contribute to their HSA, unchanged since 2017,

• HSA Contributions: Average annual individual contributions declined to $1,880 in 2021.

• HSA Investments: In 2021, 88% of accounts remained in capital preservation (money market) funds.

Maximum utility

HSA thinking has evolved to become part of an organization’s “health and wealth” rewards strategy.

One of the most valuable baseball players in any pennant chase is a “Five Tool” utility player - one who can perform at a superior level at multiple positions in the field, and at the plate. In everyday life, that’s akin to a Swiss Army Knife or a Leatherman tool.

In employee benefits, the “Five Tool” utility player is the Health Savings Account – generating superior outcomes in satisfying multiple needs:

1. Now (before retirement)—Fund current medical, dental, vision, hearing, and long-term care (LTC) out-of-pocket expenses, Consolidated Omnibus Budget Reconciliation Act (COBRA) coverage and LTC premiums,